A comparison between a gold Fund and a gold ETF

Sovereign Gold Bonds are the finest alternative to have gold in your portfolio

A gold fund and an ETF are a part of each other. When you invest in a gold fund, the gold fund further invests in a gold ETF. It just provides you with the extra convenience of investing in a mutual fund at an additional fee. Gold funds charge a fee that is over and above the expense of a gold ETF, which, at times, will reduce your return by about half per cent. So, basically, the difference is on the cost front.

But you should not consider gold as an investment. Rather you should consider it as an insurance to your portfolio so that its value will not go down when any calamity happens. If you have a time horizon of seven to eight years and want to buy gold as a fixed allocation of your portfolio, then I think the finest alternative that has been created for Indian investors is Sovereign Gold Bond (SGB). This is because all the other investment avenues, whether it is a gold fund, ETF, jewelry or even digital gold, has a markup. Even in digital gold, there is a markup of about 100-200 rupees on every 10 grams. It means that when you buy it, you will pay 100 rupees more and when you sell it, you will get 100 rupees less.

Issued by the Government of India, SGB has a eight-year tenure. They give you 2.5 per cent additional interest every year over and above the appreciation of the gold price, which is linked to the market price. So, you get 2.5 per cent additional returns instead of expenses. Also, the capital gains on maturity are exempt. So, I would say if you have that long tenure and are looking at gold as a fixed allocation in your portfolio, go for SGBs.

Product Details and attached Process Note of Sovereign Gold Bonds Scheme 2020-2021 - Series V.

Issue opening on 03rd August, 2020.

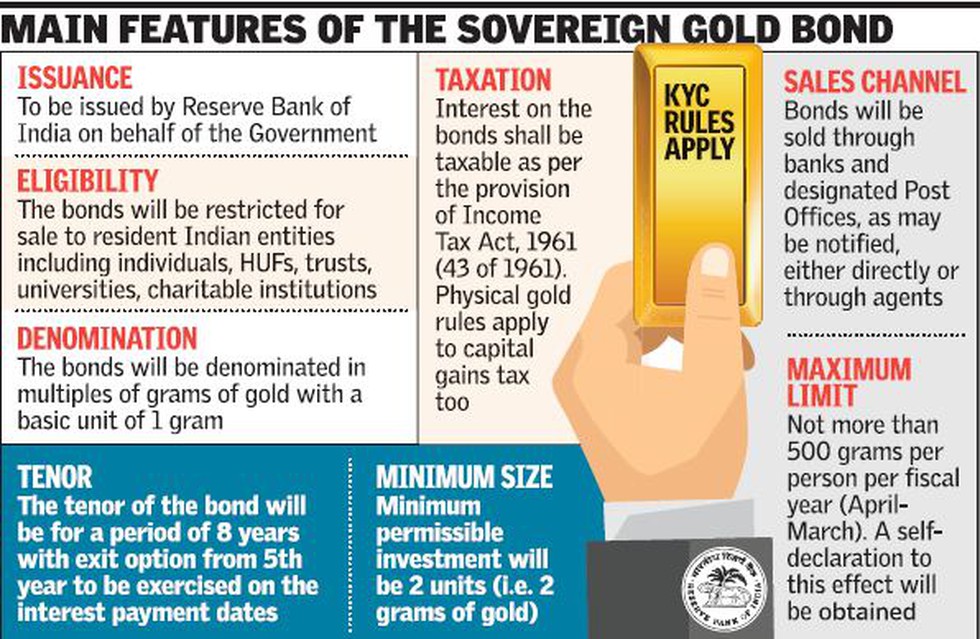

# | Details |

Product name | Sovereign Gold Bond 2020-21- Sr. V |

Issuance | To be issued by Reserve Bank of India on behalf of the Government of India. |

Eligibility | The Bonds will be restricted for sale to resident individuals, HUFs, Trusts, Universities and Charitable Institutions. |

Denomination | The Bonds will be denominated in multiples of gram(s) of gold with a basic unit of 1 gram. |

Tenor | The tenor of the Bond will be for a period of 8 years with exit option after 5thyear to be exercised on the interest payment dates. |

Minimum size | Minimum permissible investment will be 1 gram of gold. |

Maximum limit | The maximum limit of subscription shall be 4 KG for individual, 4 Kg for HUF and 20 Kg for trusts and similar entities per fiscal (April-March) notified by the Government from time to time. A self-declaration to this effect will be obtained. The annual ceiling will include bonds subscribed under different tranches during initial issuance by Government and those purchased from the Secondary Market. |

Joint holder | In case of joint holding, the investment limit of 4 KG will be applied to the first applicant only. |

Issue price | Price of Bond will be fixed in Indian Rupees on the basis of simple average of closing price of gold of 999 purity, published by the India Bullion and Jewellers Association Limited for the last 3 working days of the week preceding the subscription period. The issue price of the Gold Bonds will be ` 50 per gram less for those who subscribe online and pay through digital mode. |

Payment option | Payment for the Bonds will be through cash payment (upto a maximum of `20,000) or demand draft or cheque or electronic banking. |

Issuance form | The Gold Bonds will be issued as Government of India Stock under GS Act, 2006. The investors will be issued a Holding Certificate for the same. The Bonds are eligible for conversion into Demat form. |

Redemption price | The redemption price will be in Indian Rupees based on simple average of closing price of gold of 999 purity, of previous 3 working days published by IBJA Ltd. |

Interest rate | The investors will be compensated at a fixed rate of 2.50 percent per annum payable semi-annually on the nominal value. |

Collateral | Bonds can be used as collateral for loans. The loan-to-value (LTV) ratio is to be set equal to ordinary gold loan mandated by the Reserve Bank from time to time. |

Tax treatment | The interest on Gold Bonds shall be taxable as per the provision of Income Tax Act, 1961 (43 of 1961). The capital gains tax arising on redemption of SGB to an individual has been exempted. The indexation benefits will be provided to long term capital gains arising to any person on transfer of bond. |

Tradability | Bonds will be tradable on stock exchanges within a fortnight of the issuance on a date as notified by the RBI. |

FAQ - https://www.rbi.org.in/

Comments

Post a Comment